What is Creditworthiness

Creditworthiness is an assessment conducted by a lender (creditor) in order to determine the likelihood of a borrower defaulting on a loan.

Lenders will generally use the following 5 Cs to determine your creditworthiness:

Character: The lender will check your past credit behavior. Have you you’re your payments on time? Do you frequently change jobs and addresses? How long have you been in your current job? They’ll also check to see if you save money consistently or if you spend all your available credit.

Capacity: Can you repay the loan? The lender will review your payment history, the types of credit you have, and your debt-to-income ratio (how much of your income goes to debt repayment).

Capital: This is the money you invest in the loan purpose. For example, for a mortgage, your capital is the down payment. Having capital means you share the risk with the lender.

Collateral: This is security for the lender if you default on the loan. Examples include:

- The property itself for a mortgage.

- Investments you have, used as security for a smaller loan.

- A guarantor or co-signer who becomes responsible if you can’t pay.

Credit Report and Score: This is the most important factor. It shows your likelihood of repaying the loan and how you’ve managed past debts. It reveals if you’ve had debts in collections or sought help for debt repayment like bankruptcy or debt management.

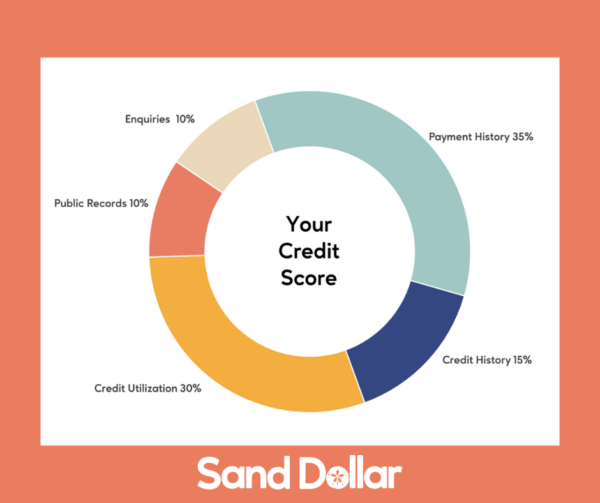

How Credit Scores Are Calculated

Breakdown of Credit Scoring Models:

Payment History (35%)

This factor looks at how you’ve repaid credit. It includes details on on-time payments, late or missed payments, public record items, and collection information.

The number of delinquent accounts relative to all your accounts also impacts your score. For example, if you have 10 accounts and 5 have late payments, this ratio may lower your score.

Credit Utilization (30%)

This factor examines the percentage of your total available credit that you’re using, particularly on credit cards and other revolving lines of credit.

It also considers your total credit limit, which is the maximum amount you can charge on a particular account.

For example, if you have a $2,500 limit on a credit card, how much of that limit you use will impact your score.

Credit History (15%)

This factor details how long your credit accounts have been open.

It includes the age of your oldest and most recent accounts.

Creditors prefer to see that you’ve responsibly managed credit over a long period.

Public Records (10%)

This includes any history of bankruptcy, collections, or other negative public records.

Such events are considered high-risk and can significantly lower your credit score.

Inquiries (10%)

When your credit file is accessed, the request is logged as an inquiry.

Only inquiries related to active credit seeking (applying for a new loan or credit card) can impact your score. These are called “hard hits.”

Hard inquiries can indicate financial distress if there are many in a short period, but not all inquiries are negative.

“Soft inquiries” (pre-approved offers or personal credit checks) do not affect your credit score.

Tips to Improve Your Credit Score

Review Your Credit Reports: Start by checking your credit reports annually from Equifax and TransUnion (the two official, nationwide credit bureaus in Canada). Ensure there are no errors or signs of identity theft. Look for unpaid balances or past-due accounts in collections and prioritize paying off these debts. Note that accounts in collections will stay on your Equifax report for six years, even after you pay them.

Pay on Time: Paying your debts on time is crucial for improving your credit scores, as payment history is a significant factor. To avoid late payments, consider setting up automatic payments or alerts to remind you to pay.

Keep Your Credit Utilization Rate Low: Your credit utilization ratio is the percentage of your available credit that you’re using. For instance, if your credit limit is $10,000 and your monthly balance is $3,000, your utilization rate is 30%. Aim to keep this rate at or below 30%. You can achieve this by spending less on credit, making more frequent payments, or requesting a credit limit increase.

Avoid Applying for Too Many New Credit Accounts: Applying for new credit accounts often results in a hard inquiry on your credit report, which can lower your credit scores, especially if your score is already low. To improve your scores, limit the number of new credit applications. Additionally, opening new accounts can reduce the average age of your credit history, another factor in your credit scores.

Keep Old Accounts Open: Try not to close old, paid-off accounts, even if you don’t use them. The average age of your accounts is a factor in your credit scores, so keeping these accounts open can help maintain the length of your credit history.

Understanding credit can help you manage your finances effectively and improve your credit score over time. If you would like to learn more about credit or how to better manage your money, please sign up for our newsletter.